You’ve been trying to budget so that you can save enough to hit that financial goal. But it never seems to have worked huh? Well, have you tried the 50-20-30 budgeting rule?

What is the 50-20-30 budgeting rule?

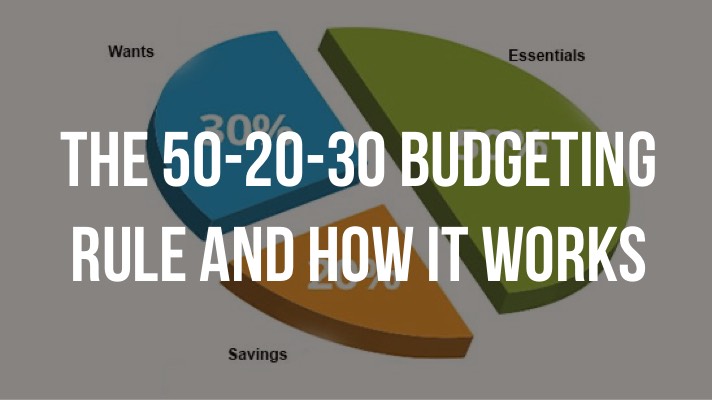

The 50-30-20 budgeting rule is a basic financial rule popularized by senator Elizabeth Warren in her book; “All Your Worth: The Ultimate Lifetime Money Plan“. This rule helps you divide your monthly after-tax income into three parts, i.e. 50% goes to your needs, 20% goes to your savings, 30% goes to your wants.

Why is budgeting important?

- Prevents overspending: Budgeting your money prevents you from spending above your income on things you do not necessarily need. When you budget, you have a articulated plan on how you want to spend your money and what you want to spend it on.

- It helps you attain your goals: When you budget you have more zeal to attain your goals. You can set aside money to achieve certain goals you set for yourself

- You save better: having a budget improves your savings habit. Now you have enough to save and plan towards your goal

- You pay debts faster: With budgeting, you can pay your debts faster. Every month you allocate money towards the debts that you owe. You don’t have to spend a good part of your life paying debts.

- It also helps improve your credit score: With budgeting you can improve your credit score. Since you don’t have to spend money on unnecessary things. This is a good way to improve your credit score

In this article, we will explain to you how the 50-20-30 budgeting rule works.

How the 50-20-30 budgeting rule works:

Step 1: Calculate your income after tax deduction

The first thing to do after receiving your income for the month is, calculate how much you have after your tax is removed. These can be state tax, local tax, income tax, Medicare etc.

However, if you’re an employee with a steady monthly income, it’ll be easy to figure out how much taxes are removed, you just need to look at your bank statements.

But if you are self-employed, your income after the tax deduction is your business expenses subtracted from your gross income. The responsibility of paying your taxes to the government is solely on you since you do not have an employer to deduct it for you.

Once you have calculated your income after tax deduction you can begin to allocate your income to the three segments, i.e. needs, wants and savings

Step 2: Allocate 50% of your now income to your needs

We all have needs that have to be met on a daily/monthly basis. However, when budgeting, it is important to keep that in mind so that you wouldn’t cut yourself short of necessities such as food, water, electricity bill, health insurance, transportation, utilities etc.

Before you begin allocating those needs you must understand and differentiate your ‘wants’ from your ‘needs’. This can be tricky especially if you are a not used to budgeting and your spending is all mumbled up. Know that your needs are things you cannot live without and are necessary for your every day living. While your wants are things you can forgo without difficulties.

To ensure that your needs are met, set aside 50% of your income after tax deduction for your needs. To make spending just 50% of your net income easy, you can set a mini-budget for your needs and allocate money to which need must be met. This helps you to stay on track and stick to your budget diligently.

For instance, if your net income is $4000, then $2000 of your income is set aside for needs. You can allocate $300 for groceries, $800 for housing/rent, $100 for the electricity bill, $100 for transportation, $500 for utilities and the remaining $200 could be for miscellaneous.

[Also see 9 Best Budget Management Apps for You]

Step 3: 20% goes to your savings and debt repayment

The next step should be your savings. Savings is very important on our journey to financial freedom. Although it doesn’t increase your wealth, it is a good place to start when thinking about your future. Your savings can be directed to a certain goal such as; retirement plan*add link*, investment account *add link* or emergencies.

Putting 20% of your net income aside and directing it to your savings account. Think of this as “paying your future self”. Eventually, your future self will thank you immensely for making such a good decision.

If you have debts, you might not want to direct that 20% to your savings just yet. Start by paying off your debts with the money and cutting down some things so you might even have just about enough to save even after all your debts are cleared.

The sooner you start paying your debts, the quicker it is to start saving and attain your financial goals. Using the hypothetical example above, since your net income is $4000, $800 goes to your savings or debt repayment if you have any.

[Also see Personal Financial hacks you need to know]

Step 4: 30% for wants

The final step is the allocating 30% of your net income to your lifestyle. As explained earlier, wants are things you can live without. You don’t need them to survive, but every now and then they enhance your lifestyle.

Your 30% can be used to buy new shoes, dining out, new clothes, Netflix subscription, gym membership, travel expenses, cable or mobile subscription etc. They are things you can forgo if you’re under a lot of financial pressure and you need to save more than your usual 20% per cent. However, your wants don’t mean that you should buy extravagance all in the name of ‘keeping up with the trend’.

After you’ve deducted $2000 for your needs, $800 for savings, you are left with $1200 to satisfy your wants from your supposed $4000 net income.

Let’s take a practical approach on how the 50-20-30 budget rule works

Laura is a 24-yrs old bank manager who is given a monthly salary of $7,000. But after a tax deduction for things like; health insurance, local tax, income tax, state tax and social security, she is left with a net income of $6,500. She goes ahead to use the 50-20-30 budgeting rule to help her track her spending and have enough to save for her retirement. She allocates $3,250 of her net income to her needs. Her needs include; electricity bill, house rent, car rental payment, utilities, groceries and other necessities.

After allocating $3,250 of her net income to her needs, she is left with $3,250. She puts away $1,300 to her 401(k)-retirement plan, which she has been building up for years. With the remaining $1,950 of her net income, she can finally buy some new clothes, renew her cable subscription, dine out with her friends and afford other nice things withing her budget.

However, with this budgeting scheme, Laura can enjoy her life and work to achieve her financial goals. But of course, with other things coming to play such as investments and various sources of income.